By Shahid Sattar | Sarah Javaid

Pakistan’s export sector is undergoing a seismic shift, one that will affect its competitive edge for years to come. The U.S. has imposed ‘reciprocal tariffs’ globally, including a 29% duty on Pakistan, as part of its protectionist policy.

The misaligned trade diplomacy – relying on the U.S. as its largest market for value-added exports while maintaining an intertwined supply chain with China – underscores how the 29% tariff is merely the first step toward a deeper economic pit that Pakistan risks falling into.

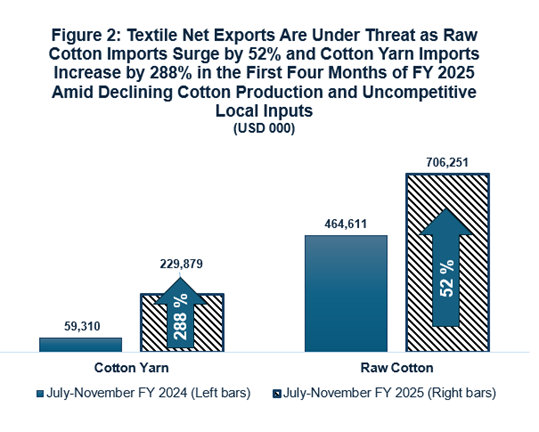

Structural inefficiencies – worsened by regressive taxation and ill-conceived energy policies – have already eroded Pakistan’s export competitiveness. This year marked a turning point when over 50% of Pakistan’s textile import bill was dominated by cotton and cotton yarn – a trend never seen before. Once a leading producer, Pakistan is now increasingly reliant on imports, with cotton yarn imports expected to surge nearly 200% and the cotton import bill projected to rise by over 50% this financial year. Together, these are projected to cost the economy a staggering $2.8 billion, with the combined total for cotton imports and textile intermediates reaching $4.4 billion.

While Pakistan sources the bulk of its raw cotton from the U.S. and Brazil, over 60% of its cotton yarn imports – cheaper than domestic yarn – now come from China, raising concerns over potential dumping and associated compliance risks.

As we officially enter the global trade war, beyond tariffs, another non-tariff threat looms: the potential for a U.S. ban on Pakistani exports.

In 2019, the U.S. banned Chinese cotton from Xinjiang over forced labor concerns, extending restrictions to any product containing Xinjiang cotton, regardless of origin.

However, through strategies such as China Plus One, transshipment, and third-country exports, China has sustained its presence and deepened its hold on the global textile supply chain. In 2024, China exported $3 billion worth of cotton intermediates to eight South Asian countries, including Pakistan, accounting for 30% of its $10.8 billion global exports in this segment.

While Pakistan didn’t directly benefit from China Plus One, it has become a key market for cheap Chinese textile intermediates, including knitted and woven fabrics, filament yarn, and cotton yarn.

Despite U.S. policies and growing supply chain scrutiny, Pakistan remains one of the largest importers of Chinese cotton yarn. And this is where the fire begins.

Pakistan’s Trade Dilemma – Cheaper Imports from China and Compliance Risks:

With a sharp decline in local cotton production, Pakistan has increasingly turned to cotton imports from the U.S. and Brazil, which now account for over 60% of total imports. In fact, Pakistan is the second-largest importer of U.S. cotton.

Simultaneously, the country has become the top importer of cotton yarn from China. This shift has strained the local spinning industry and at the same time introduced compliance risks, particularly due to the potential inclusion of Xinjiang cotton in Pakistan’s textile supply chain, especially in the absence of a traceability mechanism.

Since Xinjiang produces 87% of China’s cotton, China has redirected its (non-tradable) cotton toward textile manufacturing in response to U.S. bans. Additionally, it has implemented a tariff-rate quota system on cotton imports, ensuring that textile manufacturers primarily rely on Xinjiang cotton.

As the U.S. strengthens oversight of textile supply chains, any trace of Chinese cotton in Pakistani textile exports could result in bans in the US market for apparel.

The key question remains: What is driving Pakistan’s growing reliance on imported cotton yarn?

Price Disparities and the Absence of a Competitive Edge for Local Yarn:

The Chinese textile and apparel industry benefits from extensive subsidies. Under the Make in China initiative, the government has introduced over 900 subsidies to support local manufacturing.

In contrast, Pakistan’s textile sector faces mounting challenges, particularly following the reversal of regionally competitive tariffs and the withdrawal of zero-rating on local supplies under the EFS scheme. Power tariffs have hit record highs of 12–14 cents per kWh (the highest in the region), and the price of gas for captive power plants has surged to Rs. 3,500/MMBtu, with an additional levy of Rs. 791/MMBtu. Beyond energy costs, the rising prices of other textile inputs have further undermined the competitiveness of yarn production in Pakistan, making it increasingly difficult to compete with cheaper, duty-free Chinese imports.

China’s pricing advantage in textile intermediates is evident in its export rates. For most traded cotton yarn tariff lines, the prices offered to Pakistan are not only lower than those offered to Vietnam and Bangladesh (Table 2a), but also well below Pakistan’s domestic yarn prices (Table 2b). This cost edge enables China to maintain its competitiveness in the Pakistani market, while leaving Pakistani yarn manufacturers struggling to compete in a market distorted by cost disadvantages.

China’s Strategic Emphasis on Maintaining Low Production Costs:

The cost and pricing edge is no accident. China controls over 50% of global spinning capacity and 45% of fabric manufacturing, and in response to increasing global trade restrictions, it is doubling down on its domestic textile sector. Plans are underway to expand spinning capacity in Xinjiang and raise the cotton-to-textile conversion rate from 40% in 2024 to 45% by 2028. Generous subsidies for transporting cotton from Xinjiang to central and eastern provinces further reduce production costs and incentivize yarn manufacturers.

With this level of government support and massive economies of scale, China is able to export yarn and other intermediates at competitive prices – often lower than the prevailing prices in importing countries.

Here the challenge for Pakistan is threefold: protecting its local industry from potential dumping, managing compliance risks tied to increased dependence on Chinese imports, and securing preferential access to key export markets, particularly the U.S. and EU, where Pakistan’s value-added textiles are primarily destined.

The Current State of Cotton Yarn Imports in Pakistan:

China’s competitive edge in yarn is also visible in Pakistan’s import patterns. The most traded cotton yarn import tariff lines in Pakistan account for 100% of imports from China, which were initially subject to an 11% MFN duty (Table 3a). However, under the 5th Schedule of Pakistan Customs, these duties were reduced to 5%, and the China-Pakistan Free Trade Agreement further lowered them to 4.2%.

Moreover, exporters can access duty-free yarn imports under the EFS scheme. The combination of low export prices and 0% duty has made Chinese yarn highly competitive in the domestic market – crowding out local production.

In contrast, peer economies such as India and Bangladesh have adopted a more defensive policy posture, protecting their local industries through higher duties on Chinese yarn as reflected in their respective customs schedules (Table 3b).

A Global Snapshot:

Under WTO rules, countries can impose anti-subsidy or countervailing duties to protect domestic industries from unfair price advantages created by subsidies from trading partners.

Recently, several countries have initiated anti-dumping investigations and imposed duties in response to unfair trade practices by China.

For example, the European Commission recently imposed anti-dumping duties (26.3% to 56.1%) on Chinese glass fiber yarn imports to protect 1,200 EU jobs and restore market competition. The investigation found that Chinese imports were harming local industry.

In December 2024, India launched investigations into the alleged dumping of nylon filament yarn and trimethyl dihydroquinoline (TDQ) from China, with potential recommendations for duties.

In September 2024, Turkey initiated an anti-circumvention investigation into synthetic staple fiber woven fabrics from Malaysia, suspecting that these imports were bypassing existing anti-dumping measures on China, as the share of Malaysian imports rose sharply in 2023 and 2024.

In June 2025, Malaysia announced provisional anti-dumping duties (6.33% to 37.44%) on polyethylene terephthalate (PET) imports from China and Indonesia.

Egypt also extended anti-dumping duties on Chinese synthetic fiber blankets, maintaining tariffs of 55% to 74% until August 2025 to prevent a surge of dumped products in its market.

Urgent Call for Government Intervention to Ensure Fair Trade:

Given the global trend of rising anti-dumping measures, Pakistan faces a similar threat to its domestic industry. With heightened trade restrictions on China from the U.S., such as increased tariffs and escalating non-tariff barriers, there is a growing risk of more dumping of cheaper textile intermediates, and local manufacturers risk being priced out of their own market.

The National Tariff Commission (NTC) has previously acted decisively – even imposing anti-dumping duties on relatively low-impact products like lead pencils from China. Today, the stakes are much higher, involving Pakistan’s largest export sector, millions of livelihoods, and billions in export revenue. With the margin for error narrowing, Pakistan must take urgent and well-calibrated action to safeguard its textile industry from unfair competition.