Privatization was supposed to rescue Karachi’s power grid. However, two decades after handing Karachi Electric (KE) to private investors, the city’s homes and businesses continue to suffer from repeat blackouts, erratic billing, stalled investments and even fatalities.

As Islamabad prepares to privatise FESCO, GEPCO, IESCO, and other Discos, the Karachi experience offers important lessons to ensure the rest of Pakistan is not subjected to the horrors that have been inflicted upon 20 million Karachiites for years.

KE’s privatization was pitched as a turning point for the utility, with injection of fresh capital, private expertise and market discipline that would replace the old and inefficient state-run enterprise, and end Karachi’s decades-old legacy of chronic outages.

However, instead of steady power supply and happier consumers, Karachi has come to expect routine load-shedding, unannounced blackouts that stretch entire days, and a utility more focused on protecting profits than ensuring the lights stay on.

Impact on industry and the economy

Karachi is a central pillar of Pakistan’s economy, with its port handling over 60 percent of trade, its factories manufacturing key exports, and its services sector supporting finance, retail and hospitality industries across the country. However, under KE’s erratic supply regime, businesses and industries have to run at partial capacity or resort to expensive captive generation, slashing margins and spooking investors.

Manufacturers of everything from garments to food products wrestle with unannounced blackouts that halt machinery and damage sensitive equipment. A voltage spike during an unscheduled cut can destroy motors, ruin production batches and require costly repairs running into tens of millions of rupees for each incident. Export-oriented factories, bound by tight shipping schedules, miss international delivery windows, damaging reputations and risking contract penalties.

As per a 2024 report before the Sindh Assembly, between 2019 and 2024, at least 81 industrial units—including textile mills, sugar plants and cement factories—had shut down due to KE’s electricity crisis. Each closure translates into hundreds of jobs losses, federal and provincial revenues losses, and a shrinking industrial and export base. Remaining industries often downsize or freeze expansion plans, unwilling to risk fresh investment under an unstable power setup.

To cope, most industrial units have installed diesel generators, gas-fired captive power plants or solar arrays. These stopgap measures are expensive with fuel, maintenance, capital amortization and staff required to run the systems.

Effectively, anyone who wants to manufacture in Pakistan not only has to set up a factory but also multiple power generation systems to hedge against risks from the grid, and hence end up paying twice, once through KE’s tariff and again through backup-power costs. For a garment manufacturer operating on razor-thin margins, a heavy fuel-bill can tip profitability into fateful losses.

Moreover, recent levies on gas and furnace oil for industrial captive power generation are forcing manufacturers onto KE’s grid, where they are furnished with prohibitive connection charges and face lead times of two to three years to get the electricity. We cite the example of a major textile and apparel manufacturer with $400 million in annual exports, employing 35,000 people across different divisions.

The company has one mill under Karachi Electric with a power requirement of 15-20MW. Following the grid transition levy on gas, they shifted to Furnace Oil-fired captive generation that costs around Rs 33/kWh, compared to around Rs. 29-30/kWh on the grid and will shoot to Rs 51/kWh following the levies on FO.

The company would very much prefer to run their operations on the electricity grid under KE, as it is cheaper than FO-fired captive generation even before the levy. However, KE has quoted a cost of PKR 8 billion to provide grid connections to these units, to be paid upfront.

Additionally, they have been told that it would take about 3 years to connect them to the gird, with no guarantee of timely completion or energization. On top of this, the company would be responsible for getting approvals from several government departments (like FWO, railways, local authorities, etc.), which adds further costs and difficulties.

This situation is wholly untenable. The company cannot rely on gas or FO-fired generation for 3 years with punitive levies as it will go out of business. However, paying Rs 8 billion upfront for a grid connection with no guarantee of timely access will push the company towards bankruptcy as well. It is at a dead end, with no viable options.

While this is the story of only one company, and that too one of the largest exporters of Pakistan, the same issues are being faced by export-oriented manufacturers across Karachi. No company can afford to pay billions of rupees for a grid connection, especially without any guarantee of timely completion.

On one hand, the industry is being penalized for using alternate fuels such as gas and FO; on the other hand, it is effectively barred from accessing the grid due to prohibitively high connection charges, excessive lead times, and bureaucratic delays. It is neither reasonable nor practical for the Government to mandate grid transition while distribution companies like KE impose insurmountable barriers to achieving it.

High tariffs, billing controversies and overcharging

Karachi’s power consumers contend with some of the highest electricity rates in the country. Part of this stems from KE’s expensive power generation mix:

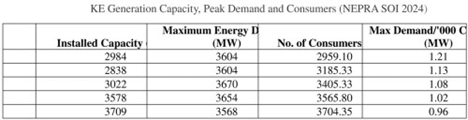

First, despite Karachi’s high peak demand of 3604MW in 2020, KE’s generation capacity stood at 2,984 MW. Between 2020 and 2024, 725 MW (or 25%) of capacity was added against an increase of 745,000 consumers (also 25%). Despite the increase in consumers, peak demand has fallen from 3,604 in 2020 to 3,568 MW in 2024, in line with the rest of the country as the economic crisis, inflation and power tariff hikes have significantly weighed down on consumer demand.

Absent the economic crisis and resulting demand destruction, at the 2020 maximum demand per consumer, KE would have experienced maximum demand of 4,518 MW, resulting in a hypothetical shortfall of 809 MW. As the economy has recovered over the past year and power tariffs have also started going down, demand is expected to recover and the hypothetical shortfall becoming real is not an unlikely scenario.

The expansion of generation capacity has lagged far behind population and industrial growth, and rather than develop new plants, KE leaned on bulk power imports from the national grid—energy whose long-term availability is not guaranteed.

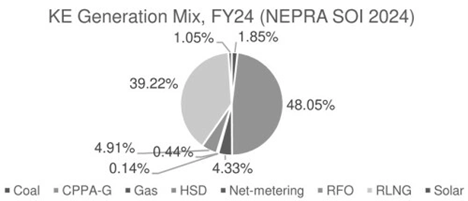

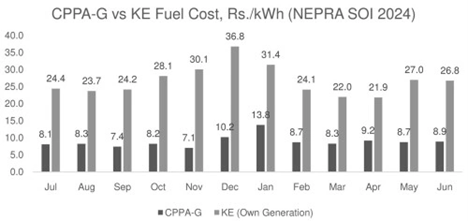

Apart from CPPA-G imports, the utility relies heavily on costly RLNG power plants and continues to run older inefficient units that drive up per-unit costs. This results in KE’s own generation—which comprises a little over half of their mix—fuel costs being two to three times those of CPPA-G during the same months:

These higher generation costs are passed directly to consumers in the form of fuel cost adjustments and higher base tariffs, burdening Karachiites with inflated bills. Despite a push from the regulator, KE has opted not to diversify their generation mix towards low-cost or renewable sources, with solar (excluding net-metering), for instance, accounting for only 1.05% of the generation mix in 2024.

There have also been instances where KE earned profits above allowable targets but failed to pass on the mandated relief to consumers. It has repeatedly used legal loopholes and regulatory inertia to avoid returning excess profits to its consumers, despite clear mandates under its Multi-Year Tariff (MYT) framework. According to NEPRA rules, when KE earns profits above its allowable return—set at 12% on its regulated asset base—it is obligated to share that windfall with consumers through reduced tariffs under a “claw-back” mechanism.

However, KE has consistently delayed these payments by either failing to file the required adjustments or taking the matter to court to stall enforcement. In 2021, for example, NEPRA calculated that KE owed consumers roughly Rs 43.6 billion, but KE challenged the order and secured a stay through court. As a result, billions of rupees in relief—some of it approved by NEPRA as far back as 2018—remain unreimbursed, even as consumers face a cost-of-living crisis.

At the same time, KE has sought massive write-offs for unrecovered consumer dues—amounting to over Rs. 76 billion during the 2017–2023 tariff period—without establishing effective recovery mechanisms or transparency. While NEPRA approved Rs. 50 billion of this amount with the condition that any future collections must be passed back to consumers, given KE’s track-record, it is highly unlikely it will honour this requirement.

Thus, the company benefits twice: once by claiming write-offs and again by retaining any future recoveries. These tactics reveal a broader pattern where KE actively exploits the system to shift financial risk onto the public while shielding its own bottom line.

These episodes underscore a trust deficit where consumers see a company quick to charge more, but very slow and litigious when it comes to giving money back. In fact, KE was also involved in the infamous over-billing scandal of July-August 2023, where NEPRA exposed billing fraud across multiple DISCOs.

Meter readings were manipulated to extend billing cycles beyond 30 days and push customers into higher tariff slabs, and phantom “detection charges” for alleged theft or meter tampering appeared without supporting meter-snapshot evidence, suggesting wilful malpractice.

KE’s own numbers tell the story: during July through December 2024, for example, it received 855,843 consumer complaints, by far the highest across all DISCOs despite serving a much smaller consumer base.

Normalising by number of consumers, KE received twice as many complaints per consumer compared to the next highest LESCO. The pattern is also apparent over time as, in FY2021-22 for instance, KE received 1,543,091 complaints, over twice the second highest of LESCO, with 768,076 complaints.

The high complaint rate highlights the prevalence of service problems under KE, with common complaints including incorrect meter readings, billing errors, delayed adjustments, and poor responsiveness in resolving issues. While it is possible that KE’s customer service infrastructure is more accessible than other Discos, the persistent complaints also point towards underlying issues remaining inadequately addressed.

Safety lapses and infrastructure failures

Beyond reliability and billing, serious safety and infrastructure issues have plagued KE’s performance, often with deadly consequences. Aging, under-maintained equipment and poor safety oversight have endangered lives and highlight the utility’s negligence in upgrading its network.

Numerous electrocutions have occurred in recent years, especially during monsoon season when stray wires and faulty equipment turn lethal. In FY23, for example, 33 people died due to electrocution in KE service areas. Following an investigation of these incidents, Nepra attributed one fatality (a lineman’s death) to direct negligence on KE’s part, having failed basic safety protocols like not properly isolating high-voltage lines while work was being done, inadequate site supervision, and conducting work in an unplanned and haphazard manner. It imposed a fine of Rs 10 million on KE as a result and ordered compensation of Rs 3.5 million to the family of the victim.

“Privatisation should have financed grid modernization with upgraded transformers, insulated cables, remote monitoring and rapid-response crews. Instead, KE’s network shows signs of chronic underinvestment as overloaded feeders trip frequently, and announcements of high-voltage line upgrades or smart grid projects often stall after initial fanfare.”

Lack of adequate transmission capacity is in fact one of the reasons KE has to rely on costly RLNG-based generation while cheaper generation capacity under CPPA-G goes unutilized, causing Karachi’s power consumers to face much higher costs than the rest of the country.