Shahid Sattar and Ureeda Majeed

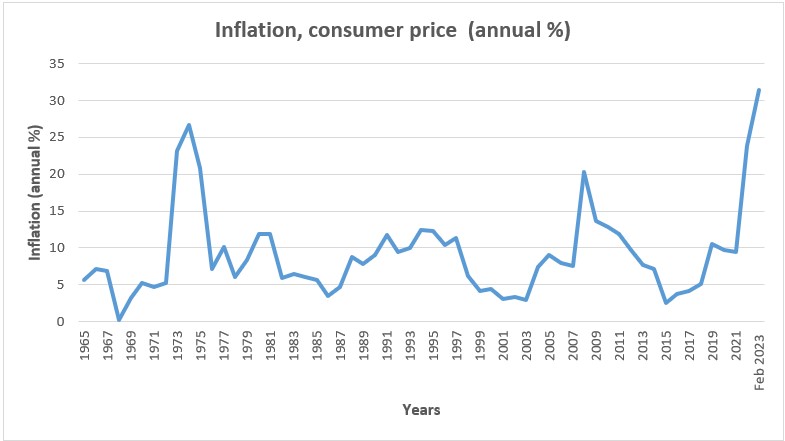

Imagine living in a country which sees an annual food inflation of over 50%. Currency collapse or the daily price change for many developing and underdeveloped countries is now a reality. For such countries the fall in their local currency versus the dollar adds to inflation and as a lot these countries import most of their oil and gas they suffer from the double impact of rising energy prices and high exchange rates. Pakistan’s inflationary situation is no different. Inflation last month surged to 35 to 36 %, its highest level since 1974, according to the latest figures released by the PBS and the Finance Division has predicted inflation to remain high, and may even increase further due to market frictions caused by demand and supply gap, exchange rate depreciation and high prices of fuel and energy.

While traditional economic policies of the west fail to counter inflation in Pakistan, it’s not the only country battling this fate. The Turkish lira had lost its value even before the pandemic began. It lost more than 40% of its value in 2021. Surprisingly Turkey still successfully managed the crises and stood among a few countries noting a positive growth rate for the year 2020. Post pandemic, the lira crises drove up the import prices aggravated by Russian war in Ukraine hiking Turkey’s energy and import bills.

In Feb 2023 the average inflation rate in Tukey was 55.2%. This intense inflation of Turkey is attributed to the unconventional strategies adopted by the Turkish government. Unlike the central banks around the world raising the interest rate to bring down soaring inflation under control, in Turkey the spiraling inflation is tied to government’s efforts to fundamentally overhaul the economy, keeping the interest rates low in hopes that this will stimulate the economy and increase production.

Turkey’s economic policy is in contrast to the laws of traditional economic theory that has not been working well for quite some years now. May be the tradition laws of economics needs to rewritten or may be the economy of turkey is an anomaly however this strategy of keeping interest rates low now seems to have run its course and may not work well for Erdogan’s popular support and there seems little he can do in the coming days to reverse the downslide. As of Feb 2022, the Turkish government decided to address the rising inflation by reducing the value added tax (VAT) on basic food items. In addition, in 2021, the government provided the most impoverished with energy subsidies to the value of 12.2 billion $ thus aiming to support 50% of the price of natural gas and 25% of the price of electricity. In Dec 2021, the government also raised the minimum wage by 50% to help the struggling citizens.

The woes of the Pakistani rupees are not that different from the Turkish lira. Similar to Turkey Pakistan’s economy is heavily dependent on imports, high inflation and devaluation of currency which in combination are fast eroding the purchasing power of the minimum wage, public sector salaries and pensions. Keeping all the economic jargon, unorthodox policy and politics aside how do people actually handle inflation as high as 50% in these economies in which it seems prices are not determined by market forces but sheer speculation about exchange rate and devaluation. Today if one buys a dozens of eggs for Rs 238, two days later they may be buying them for Rs 350 and the reason of this price hike can be anything from high cost of chicken feed, high transport cost, high fuel cost, high electricity costs, war in Ukraine to ineffectiveness of the past governments. The inflation itself becomes the cause of more inflation. A vicious cycle of satanic hyperinflation. If the price of household items such as milk, eggs, sugar and the flour are changing daily what’s a bakery to do. If we move up the scale complex enterprises and big businesses with multiple inputs and costs how do, they survive inflation. As a consequence of high inflation and with local currency losing value continuously it is not a surprise that even a street hustler of Istanbul sells his fake branded merchandise in dollars.

Since the abandonment of the gold standard and the Brettonwood Agreement developing nations have been desperately looking for ways to stabilize their domestic currency and ensure economic stability and prosperity. For majority of these countries one way of to stabilize their local currency is to peg the local currency to major convertible stable currency (which is dollar). The dollarization process can be partial or complete (full dollarization or currency substitution). The idea of using a stable means of transaction for trade make sense as Individuals want to maximize their purchasing power and protect their money / asset from shocks due to economic and political instability and depreciation especially if your currency is losing value 3 to 4 times a day.

Irony is that dollarization for smaller and less developed countries is the ability to trade in

currency that’s is stronger and more internationally recognized hence Trade becomes more stable and less prone to market volatility. In the long run it can encourage more international businesses to set up local offices to take advantage of the stable currency and help the local economies develop quicker. Developing countries become larger international players and the Balance of Payment is less prone to recurrent crises. Dollarization encourages FDI and as a whole financial and investment industry benefit from dollarization. It reduces the country’s risk thereby providing a stable and secure economic and investment climate. The diminished risk encourages both local and foreign investors to invest money into the country and the capital market and the fact that an exchange rate differential is no longer an issue helps reduce interest rates on foreign borrowing.

Many emerging markets economies already use dollarization to some extent. The financial/banking system of Panama for instance is a fully institutionalized dollarization, no exchange controls, or restrictions on the movement of capital, readily accessible credit with sophisticated lenders who are well known both locally and internationally and an active and modern capital market. Zimbabwe legalized the generalized the use of dollars in 2009 and later suspended the use of its local currency in 2015. This

reduced inflation, increasing it citizen’s purchasing power and increasing economic growth. However, it also meant that Zimbabwe had no control over its own monetary policy. In 2019 Zimbabwe reversed its decision and reintroduced its own Zimbabwe dollar and outlawed the use U.S dollar. In response to hyperinflation Bolivia underwent dollarization in early 1980’s. Dollarization paired with fiscal contractions allowed the country to control inflation and later in 1994 Bolivia transitioned to pegged regime with intentions to de-dollarize. European countries except UK and Switzerland accept Euro as their only legal tender replacing their own currency since 2002. Cambodia has dual currencies. The urban economy is governed by USD and the rural economy by their domestic currency Riel. Nepal and Bhutan use Indian Rupee and their domestic currency follow fixed currency peg.

What interesting in case of Turkey is that the country has found this unique balance between in Lira and international currency (Dollars or Euros). With a huge number of Doviz (currency exchanges) the shoe leather cost is minimum in the capital where official currency remains Lira while the currency in circulation is dollar. Workers are paid wages adjusted to international dollar. All business enterprises either accept dollars or euros or liras equivalents.

In a country like Pakistan where the people are rich and government is poor it’s not a surprise that there is often a high demand of dollars or dollars trading is being carried out in the black market.

Individuals want protect their money from losing value. In Pakistan there are generally three safe investments Gold, real estate and third foreign currency. It’s not a surprise that in Pakistan like all developing countries unofficial rates of dollar is high with frequent shortage of dollars in the market. The demand of dollars in the market will continue to increase as people want to hold onto a currency which is stable and is not under constant threat to lose its value. Multinationals are already paying their employees dollar equivalent wages. Overtime the businesses and enterprises in Pakistan are more likely to trade in dollars if they aren’t doing so already. In order to keep up with frequent price hikes, high interest rates and increasing energy bill it is only a matter of time before more people in Pakistan will want to be paid in dollars or at least in dollar equivalent inevitably pushing the Pakistani economy towards dollarization. The real question remains Do we really want to move in this direction?

Figure 1: Water conservation progress of US Apparel and Textiles

Figure 1: Water conservation progress of US Apparel and Textiles

Figure 1: Performance comparison of Sarena Textile Industries

Figure 1: Performance comparison of Sarena Textile Industries

Source: APTMA

Source: APTMA