The Snake Bites Once Again – Energy

Shahid Sattar and Amna Urooj

The persistent deviations and inefficiencies in Pakistan’s energy sector have generated extremely negative impacts on both end-users and enterprises, stalling the country’s pursuit of sustained economic development. The textile industry, which constitutes a significant proportion of exports (60%), manufacturing sector employment (40%) and banking credit (40%), is acutely impacted by the high energy tariffs and circular debt crisis, requiring prompt attention to ensure stability in exports and employment.

Source: APTMA

Source: APTMA

The textile sector is grappling with a severe lack of gas and RLNG, due to rapidly declining gas reserves and escalating limited import of RLNG due to high prices caused by the Ukraine situation. This shortage is unlikely to improve in the near future. As a result, the industry is turning more to electricity from the grid, despite its various challenges, such as lack of steam and dependability. For the textile sector to remain competitive, it is crucial that the cost of electricity in the region remains reasonable. The government had pledged a Regionally Competitive Energy Tariff (RCET) of Rs 19.99/kWh for EOUs until June 2023, but due to the ongoing economic turmoil and IMF negotiations, this RCET, has currently been cancelled starting March 2023.

Ironically, an analysis of the cost of service for B3 & B4 industry and that too as per data provided by CPPA/NEPRA, reveals that in actual the provision of a 9 cents/kWh taris involves no subsidy as can be seen below for FY22. According to CPPA/NEPRA calculations, the cost of electricity is 8.1 cents and excluding cross-subsidies plus transmission and distribution cost makes a total of 9.3 US cents/kWh.

Cost of Service for B3 & B4 Industry as per CPPA/NEPRA

It is also worth mentioning that the Small and Medium Enterprise (SME) sector, who do not have alternate energy sources, can face severe economic consequences due to withdrawal of regionally uncompetitive tariffs. The intense competition in the global export market and the crucial requirement for Pakistan to uphold or potentially increase its exports calls for caution in the context of elevated electricity charges. The SME sector is already at a disadvantage due to the absence of subsidized credit, difficulties in accessing import for re-export plans, and the incidence of multiple tax duplications. The imposition of higher electricity tariffs is likely to result in cost escalation, rendering the SMEs incapable of remaining competitive in the marketplace both for exports or local consumption as imports become relatively cheaper.

On the other hand, the non-implementation of the Textile Policy 2025 implies that the business environment in Pakistan is not conducive to the growth of both existing and new investors. Consequently, textile enterprises in Pakistan have become regionally uncompetitive in comparison to their counterparts in South Asian countries such as India and Bangladesh, resulting in an adverse outcome of the aforementioned factors. The economic losses arising from the aforementioned factors, both current and future, are significant and alarming.

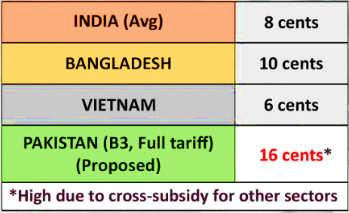

Energy Tariff’s Across the Region

Source: APTMA

The issue at hand is: despite the potential for much higher exports by the textile industry through favorable policies and tariffs, the government’s inaction on this front remains inexplicable. It may be that policymakers and decision-makers are not fully cognizant of the benefits associated with such decisions or lack a precise understanding of the actions necessary to save the sector from collapse. Alternatively, it is possible that the industry is not adequately communicating and emphasizing these concerns. Nonetheless, APTMAs consistent efforts in promoting RCET have been instrumental in the past, creating a positive impact.

As a matter of fact, reliance on grid electricity at over Rs. 40/kWh makes the Punjab industry uncompetitive in international & local markets thereby, shifting the available orders to cheaper alternatives internationally as well as within Pakistan. This will consequently further break the already broken economic position of the country via unemployment, lower exports and bankruptcy. And now that it is evident that the withdrawal of RCET OF Rs 19.99/kWh and a gas tariff of $9/MMBtu for gas/RLNG in Punjab will result in closure of Punjab based textiles. Immediate intervention to correct injustice is requested from the policy makers as Pakistan can not afford further deterioration in the balance of payments which may amount to a loss of $10 Billion exports per Annum.

The revocation of RCET will render more than 50% of Pakistan’s installed capacity in the Punjab-based industry non-operational. Meanwhile, the Sindh-based industry will maximize gas usage, which costs 4 cents or Rs.11 per kWh, with added steam and hot water benefits. The cost of self-generation for Punjab-based industries using gas/RLNG will be 11.5 cents or Rs.31 per kWh. Additionally, grid electricity is both uncompetitive and unreliable, reducing effective production capacity by over 25% due to substandard supply. Furthermore, gas supply to the export sector in Punjab is severely restricted, meeting only 25% of the demand and only available to selected units when it is available at all.

Energy Differences Across Punjab and Sindh

Source: APTMA

This dolorous situation implies that the $5 Billion investment over the last three years that resulted in increased exports by a massive 55% in two years i.e., from $12.5 Billion in 2020 to $19.5 Billion in FY22 through the provision of RCET and Temporary Economic Refinance Facility (TERF) will all be lost.

During periods when the government provided regionally competitive energy tariffs, the Export Oriented Industries (EOIs) demonstrated the crucial role of these tariffs. This was evidenced by an immediate increase in production, reaching full production capacity, creating new job opportunities, attracting new investments, and leading to the full operation of all mills. It is unquestionably a sustainable path to economic growth to enhance trade competitiveness, as it is not subject to any liability, unlike aid. Additionally, tying hopes of economic growth to remittances is unreliable, as the long-term trajectory of remittances is unpredictable. Countries that have achieved economic growth and sustainable development prioritize export-led growth as their top agenda.

Another important aspect to consider is that when the Government of Pakistan borrows from the international bond, it typically does so on an interest rate of 7% – 8%. While foreign loans can provide much-needed financial resources to the government, their cost in the form of interest payments and debt servicing is a drain on the country’s resources, limiting the government’s ability to spend on critical areas such as healthcare, education, and export-led growth.

Cost of Regionally Competitive Energy Tariffs (RCET) to Textile Sector

Source: APTMA

In fact, depending on export-led growth is way better than any reliance on foreign loans and aids. When compared technically; the total cost of RCET as a percentage of textile exports from FY19 – FY22 was just 2.67%. Growth led export policies such as RCET can lead to increased exports and higher revenues for the industry against foreign loans with an interest rate of 7% – 8%. The difference in interest rate of external borrowings vs cost of RCET has significant implications for the government’s finances, saving billions of rupees as the government doesn’t have to repay for the later one.

On the other hand, one alternative solution to insulate SMEs from high energy tariffs, without violating any World Bank or International Monetary Fund conditionalities for subsidies, would be establishing an RLNG-powered or coal fired generation facility, aimed at catering to the energy demands of the textile industry. As a complementary initiative, exploration of the feasibility of setting up off-grid solar and hydro power plants in KPK to reduce operational expenses is also possible. However, this too has its own set of problems such as wheeling charges, stranded cost and cross-subsidy, issues of electric supply from grid, notice period, and solar net-metering CAP.

One of the challenges in establishing a power plant dedicated to serving Export Oriented Units (EOUs) in the Textile industry is related to the definition of open access/wheeling charges. With the discontinuation of subsidies, the industry must use the Competitive Trading Bilateral Contract Market (CTBCM) to remain competitive. In this context, the two disputed components out of the five components of the wheeling tariff, namely cross-subsidy and stranded cost, must be waived for EOUs. In order to remain competitive in the international market, the wheeling charge must exclude cross-subsidies and standard. Additionally, the current power wheeling system is inadequate for the CTBCM regime, and the supply of electricity is compromised as it does not conform to the grid and distribution codes established by the Government of Pakistan.

Pakistani policymakers need to prioritize sustained export-led growth to promote economic independence and overcome debt accumulated from loans and relief packages. A strong export base provides a self-sufficient and highly beneficial approach to strengthen the economy, free of any conditionalities. The ultimate aim is to achieve economic and political independence in Pakistan, free from reliance on goodwill or aid.

Related Articles:

- Ladder and the snake – https://www.brecorder.com/news/4694689/ladder-and-the-snake-20190522477837

- The snake has truly bitten – https://www.brecorder.com/news/4704478/the-snake-has-truly-bitten-20190702493518