The Eighty-Twenty Rule for Maximizing Foreign Exchange Earnings

Dr. Gohar Ejaz

Pakistan’s economy has been facing a number of challenges in recent years, including low growth, high inflation, large fiscal and current account deficits, and declining foreign exchange reserves. Despite various efforts to spur economic growth, the country’s GDP growth rate has remained relatively low, averaging around 3-4% in recent years.

In the last 5 years, Pakistan has received a total of $32 billion as loans from various sources including China, Saudi Arabia, Abu Dhabi, World Bank, and the Asian Development Bank. In contrast, Pakistan has while earned $140 billion from exports. Expats have contributed $140 billion as worker’s remittances to the country during the same period. Given these inflow volumes and the eighty-twenty rule, Pakistan should focus on these two sectors aligned with relative weights of the expected outcome.

Composition of Foreign Economic Assistance, Remittances and Textile Exports (USD Million)

* Of which, 2500 Million USD is part of cyclical one time facility by ADB and 500 Million from AIIB Special Fund.

**State Administration of Foreign Exchange (SAFE) Authority, China.

***Saudi Fund for Development (SFD) Time Deposits.

Both exports and worker’s remittances are important sources of foreign currency for Pakistan and play a crucial role in its balance of payments, contributing 80% of total forex revenues. However, the relative economic importance of these two sources is significantly different where exports contribute directly to GDP growth, employment generation and provide the only sustainable long-term solution. Worker’s remittances on the other hand provide limited and indirect support to the GDP, as well as employment and are not considered as preferential source of forex.

Pakistan’s exports have seen an upward trend especially during FY20-FY22 where textile exports grew by a phenomenal 55% in just two years. Worker’s remittances also posted a growth of 50% in these two years but are dependent on the world economic conditions especially the state of the economies from which they originate and hence not considered stable or sustainable in the long run.

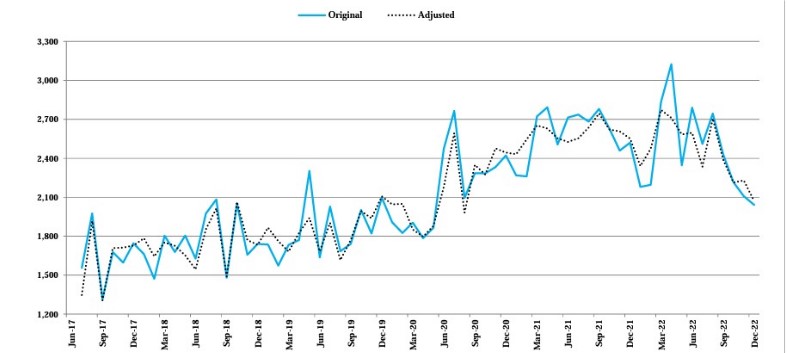

However, the state of remittances as well as exports is now depicting an alarming future. During H1 of the current fiscal year, remittances from 10 European Union countries (including Italy, Spain, Germany, France and Greece) sent to Pakistan showed negative growth. The number of remittances from EU member countries decreased from $1.750 billion in the same period of the previous fiscal year to $1.544 billion, representing a decrease of 11.77%.

Remittance Inflow (Jun’17 – Dec’22) in USD Million

Source: State Bank of Pakistan

With continued socioeconomic turbulence, Pakistan has always been relying on Foreign Economic Assistance (FEA) in various forms. FEA refers to government aid aimed at enhancing the economic growth and well-being of developing nations. This aid can take the form of concessional loans, grants, and technical support, and may be provided by both bilateral sources and multilateral organizations such as the World Bank, Asian Development Bank (ADB), Islamic Development Bank (IsDB), Asian Infrastructure Investment Bank (AIIB), or United Nations (UN).

Pakistan has had a history of being heavily dependent on FEA since its inception, which is not an ideal situation for a country’s long-term economic growth and development. There are several reasons for this:

First, reliance on FEA often leads to a lack of fiscal discipline and weak revenue collection efforts. Governments tend to rely on external aid to finance their spending, which can lead to large fiscal deficits and a buildup of government debt over time.

Second, FEA can create a culture of dependence, where the recipient country becomes reliant on external aid for its development and growth. This can lead to a lack of incentives for domestic reforms and a reduction in the country’s capacity to generate its own resources and finance its own development.

Third, FEA can distort the local economy by providing resources to sectors or projects that may not be aligned with the country’s domestic priorities or economic strengths. This can create a misallocation of resources and reduce the overall efficiency of the economy.

Fourth, FEA can also have negative impacts on the country’s currency, as large inflows of foreign aid can lead to an appreciation of the local currency and reduce the competitiveness of the country’s exports.

Pakistan attracted more than $25 billion in the real estate sector in 2021. According to a research study, 25-30% of remittances went into the real estate sector while 21-22% from the Roshan Digital Account were invested in the sector. Traditionally, expats have invested in real estate sector of Pakistan through remittances. A slowdown in the real estate sector necessarily negatively impacts investments and remittances. Remittances have decreased drastically over time, increased tax on property being the primary reason. Previously, even resident Pakistanis used to invest their savings in the real estate sector, however, exorbitant property tax rates have forced them to spend their savings in buying gold, and/or dollars, thus parking their funds in non-productive assets. In order to reverse the decline in worker’s remittances, overseas Pakistanis including non-resident persons may be exempt from advance tax payable under section 236K of the Income Tax Ordinance 2001 on the purchase of immovable properties in Pakistan. Expats may only be liable for Advance Tax on Sale/Transfer under section 236C of the Income Tax Ordinance 2001. This way remittances can be augmented to uplift Pakistan’s economic growth.

Focus on export growth necessarily involves promoting textiles as this sector contributes 62% of all exports. Pakistan’s textile industry, however, is facing a major crisis as it is rapidly losing credibility and competitiveness in the global market. The $19.3 billion industry, which relies heavily on exports, is experiencing a decline in global shipments. This situation is causing concern among its loyal international customers, who are becoming increasingly skeptical about the industry’s ability to meet deadlines and fulfill orders in a timely manner. The situation is further compounded by the shortage of dollars and basic raw materials, including cotton, dyes, and chemicals, which is causing many exporters to hesitate when booking new orders. As a result, the future of the industry looks uncertain, and unless measures are taken to address these challenges, the textile sector in Pakistan may continue to face a downward spiral.

Falling Textile Exports (USD Billion) – Targeted vs Expected in FY23

*Provisional-based on current trend.

Source: Author’s Own

Expanding our exports especially in the textile sector and removing all hurdles for remittance inflows should be of utmost importance. No doubt, we should also continue to maintain strong relationships with our current lending partners and work towards attracting investment from new sources. However, time has now come to consider that despite the current challenges faced by Pakistan’s textile industry, it is crucial that immediate steps are taken to re-invigorate the sector. Some of the critical steps are:

The cost of conducting business in the textile sector has become unmanageable due to the elimination of Zero-Rating (SRO 1125) and the implementation of a 17% GST on export-oriented industries. The high sales tax has led to an increase in working capital and interest rates, causing a surge in smuggling, fraudulent activities, and the import of second-hand clothing. To alleviate the situation and secure working capital, it is imperative to immediately reinstate Zero Rating for the entire textile sector through SRO 1125.

Address the looming liquidity crisis in the textile sector of Pakistan, caused by factors such as non-release of funds, high taxes, increased competition, and high energy costs. It is imperative to release all held-up funds such as deferred sales tax, TUF etc. as well as enhance working capital limits in accordance with rupee devaluation and increasing textile exports.

Moreover, in order to ease the liquidity crisis and avoid defaults, moratorium on capital repayment from July 1st, 2022 to June 30th, 2023 may be implemented during the period of this financial hardship to allow the industry time to stabilize and recover.

The current allocation of gas resources in the economy is unsustainable. To secure a sustainable gas supply and improve competitiveness, the priority of gas distribution to various sectors needs to be reevaluated. Priority should be given to productive sectors such as textile industry, with a focus on export-based industries over the domestic sector. This strategy would lead to increased exports, improved competitiveness, job creation, and a positive impact throughout the value chain. The current pricing disparities and promotion of non-productive use of limited resources in the gas sector should be addressed through reforms, such as the weighted average cost of gas (WACOG) and pricing that accurately reflects the economic value added through gas.

The maintenance schedule for industrial feeders disrupts 25% of the industrial production of businesses and negatively impacts industrial production and exports. The country is already facing low exports and industrial production, making it crucial to improve the quality of electricity supply. To address these issues, it is imperative to redouble efforts to improve the quality of electricity supply and mitigate the negative impact on industrial production and exports. The long-standing issue of provision of RCET’s to the entire textile value chain needs to be also resolved expeditiously. Likewise, the assessment and announcement of reasonable open excess charges of power (Wheeling) should also be promoted while it is also important to enhance the limit of 1 MW on solar to 5 MW for industrial net metering for promotion of alternative energy supplies. Increasing the limit of 1MW will also contribute to the economy by receiving the burden of setting up new solar plants providing them Take or Pay contracts and killer sovereign guarantees. The government must reconsider its decision to sponsor new solar projects given this very real alternative.

The curtailment on import of raw materials and spare parts has resulted in an acute shortage of both. This has led to non-maintenance of machinery, breakdown and running out of raw material leading to closure of textile mills. Urgent corrective action is needed.

To achieve economic and political independence, Pakistan must focus on its textile industry to get out of the debt cycle it is stuck in. To do this, it must prioritize adding value to its exports, especially in the highly productive textile sector, through supporting higher value addition. Investment and improvement in production and export capacity is crucial and requires a long-term textile policy and access to energy resources. Increasing exports will also help create jobs and prevent social and economic unrest.

In conclusion, while FEA can provide valuable resources for a country’s development, a heavy reliance on it can lead to a number of negative consequences for a country’s economy. It is important for countries to strive for greater self-reliance and to implement reforms that increase their own resource generation and strengthen their domestic economies. It is clear that the need for credit reoccurs regularly and that it is time for the country to consider reforms to break the cycle of debt and aid. Domestic initiatives and a genuine process that focuses on ground realities are crucial for implementing true and meaningful change.