By Shahid Sattar | Absar Ali

On Tuesday 28th November, power regulator Nepra will hold a public hearing on the Discos’ petitions to determine a ‘Use of System Charge’ for power wheeling under B2B contracts. A seemingly routine matter, this determination will, however, define Pakistan’s economic trajectory for years to come.

For context, the National Electricity Policy allows for a Competitive Trading Bilateral Contract Market (CTBCM) where bulk power consumers can directly purchase electricity from competitive power producers and use the government’s transmission and distribution system to transport it from the point of generation to the point of usage. The Use of System Charge (UoSC) is the “price” such consumers must pay to use the transmission and distribution system.

The export sector has long advocated for this to overcome prohibitive power tariffs that render manufactured exports internationally uncompetitive and are a barrier to not just export growth but also foreign and domestic investment in export-oriented activities.

Pakistan’s power sector is characterized by a single-buyer model where the government purchases electricity from different power producers and distributes it to final consumers at self-determined prices.

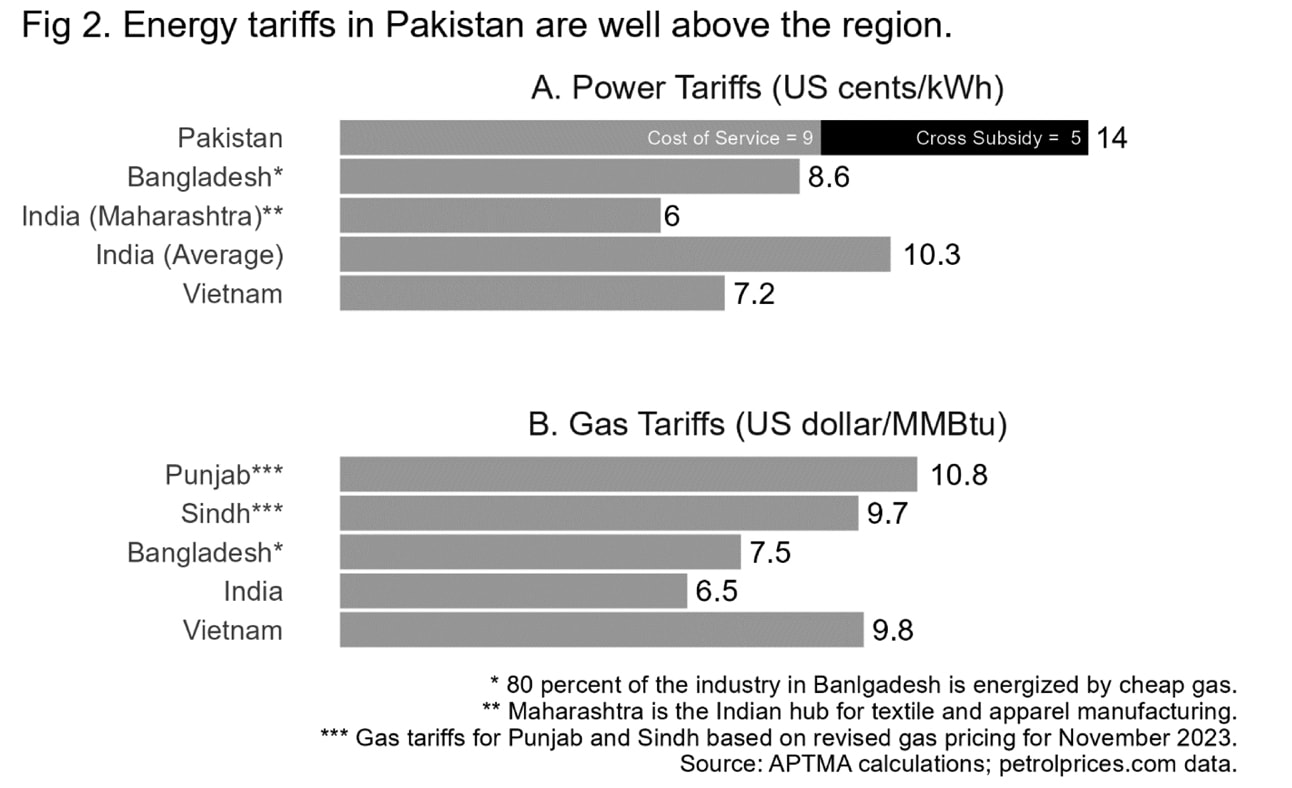

The grave issue with these prices is that in addition to the actual cost of generation and service, they include various economic inefficiencies like inter- and intra-DISCO cross-subsidies that make power tariffs for industrial consumers in Pakistan almost twice the average tariff for competing firms in the region (Figure 1).

To achieve regionally competitive energy costs ideally requires a separate power tariff category for exporters based on the actual cost of service, excluding all forms of taxation and other distortions. B2B power contracts with a UoSCat 1-1.5 cents/kWh to cover the transmission and distribution costs incurred by Discos can also achieve the same objective without any subsidies from the government.

If allowed, this would rid the export sector of prohibitive distortions in power tariffs and significantly boost export competitiveness.

Estimates suggest that annual exports could increase by up to $9 billion annually by facilitating closed production units to reopen and operationalizing additional capacity already installed under export financing schemes but sitting idle due to high energy costs. It will also create a favorable business environment to stimulate fresh investment in further expansion and upgradation of production capacity to add another $20 billion to annual exports.

In this regard, Nepra has solicited petitions from the DISCOs for the determination of the UoSC. What the DISCOs have proposed, however, can be described as preposterous at best(Table 1).

Table 1. DISCOs’ proposed UoSC for hybrid consumption.

============================================================================================

LESCO FESCO GEPCO HESCO IESCO MEPCO PESCO

============================================================================================

Industrial B3 Consumers

============================================================================================

Energy Cost 0.00 0.28 0.71 1.20

Capacity Cost 8.73 8.75 10.12 13.65 5.87 6.21 11.70

Transmission Charges 0.70 0.71 0.81 1.10 0.47 0.50 0.90

Distribution Charges 1.13 1.37 2.93 4.22 1.37 1.26 2.20

Total Applicable Costs 10.56 10.83 13.87 18.97 7.99 8.67 16.00

Impact of Losses 1.27 0.92 2.68 0.32 0.83 2.70

Total Cost of Service 11.83 11.75 13.87 21.65 8.31 9.50 18.70

Cross Subsidy 5.58 6.74 6.93 10.37 7.06 15.56 5.20

Proposed UoSCRs./kWh 17.41 18.49 20.80 32.02 15.37 25.07 23.90

Proposed UoSC cent/kWh 6.11 6.49 7.30 11.24 5.39 8.79 8.39

============================================================================================

Industrial B4 Consumers

============================================================================================

Energy Cost 0.00 0.07 0.09 1.23

Capacity Cost 8.58 8.53 10.12 16.93 6.14 7.00 12.62

Transmission Charges 0.69 0.69 0.81 1.36 0.56 0.56 1.02

Distribution Charges 0.88 0.66 2.93 2.70 2.03 0.79 1.93

Total Applicable Costs 10.15 9.88 13.87 20.99 8.80 8.44 16.81

Impact of Losses 0.26 0.16 0.62 0.08 0.11 0.40

Total Cost of Service 10.41 10.04 13.87 21.61 8.88 8.55 17.21

Cross Subsidy 7.40 9.50 7.35 10.34 7.25 16.58 6.81

Proposed UoSCRs./kWh 17.81 19.54 21.21 31.95 16.13 25.13 24.01

Proposed UoSC cent/kWh 6.25 6.86 7.44 11.21 5.66 8.82 8.43

============================================================================================

Rs. 285 = $1 assumed for conversion to US cents.

Source: DISCOs’ petitions for determination of UoSC as published on NEPRA website

============================================================================================

Taking B3 industrial consumers as an example, the DISCOs propose a UoSC ranging from 5 cents/kWh to 11 cents/kWh. Not only is this around as much and in some cases higher than the average cost of generation and service at 9 cents/kWh in Pakistan, but also much higher than what firms in competing economies are paying for power generation, transmission, and distribution (see Figure 1).

What is even more appalling is that no basis or justification behind the application of cross-subsidies—mathematical or otherwise—has been provided, except by LESCO, which specifies that:

“Undoubtedly, the consumer price should reflect the real cost of the generation, transmission, distribution, and supply of electric power to allow the fullest recovery of the legitimate cost for the provision of the electricity. However, where the same is not possible for any reason whatsoever then the cost for the provision of electricity is recovered in a manner that the consumers who can pay the high cost pays for the high prices which supports the other consumers.

The eligible BPCs are the consumers of 1 MW or more of the power. Generally, such BPCs are the industries who actually pass on the costs.” (LESCO petition for UoSC determination, as available on the NEPRA website) Several points require emphasis:

First, this statement concedes that cross-subsidies paid for by industrial consumers are undefined and untargeted. It acknowledges that consumer prices should reflect the real cost of generation, transmission, and distribution, but when this is not possible “for any reason whatsoever” the cost is recovered through cross-subsidies.

This implies that the cross-subsidy is not necessarily directed towards lifeline or protected consumers as it has been made to believe. Rather, it is effectively a subsidy to the DISCO when and where it fails to conduct its most basic task of recovering the amount for which it has sold electricity for “any reason whatsoever”.

Second, the cross-subsidy is paid on the principle of “who can pay the high cost pays for the high prices which support the other consumers”. Apart from the obvious issue that DISCOs have no expertise or jurisdiction in deciding who can or cannot pay for the high costs, the indiscriminate application of cross-subsidies across all industrial consumers is in contradiction to this objective.

Third, the assumption that generally consumers who can pay the high costs are “industries who actually pass on the costs” is problematic in every conceivable manner.

Broadly, industries can be categorized into non-traded and traded sectors.

Non-traded sectors are those that cater to the domestic market. Firms in these sectors pass on the impact of power sector inefficiencies and the government’s own welfare obligations to domestic consumers at the cost of consumer welfare. Because the cross-subsidy is applied indiscriminately to all industries across the country, it is paid for by all consumers of any goods manufactured in Pakistan.

Effectively, this is an extremely inefficient and unequal form of taxation, much like sales tax, that is paid for in the same manner by rich consumers and poor consumers, those buying essential commodities or non-essential commodities, no matter what.

In the case of traded sectors, it is even more problematic. Unlike non-traded firms that receive heavy protection through import duties and other restrictions and, therefore, have the ability to pass on the impact of higher energy costs to consumers, export-oriented firms must compete in international markets where competition is fierce and on price.

These firms cannot pass on the impact of higher energy prices because consumers can simply substitute their products with those of competing firms in regional economies with lower energy costs and lower prices. For traded sectors like textiles and apparel, on which the entire economy depends to generate foreign exchange earnings — the shortage of which is the fundamental issue behind every economic crisis Pakistan has faced — cross-subsidies in power tariffs take the form of a tax that cannot be exported.

But this logic seems to be completely lost on our policymakers. It was reported in a newspaper on November 21st that the power division has shown a reluctance to propose to operationalize the CTBCM model because it would mean an end to the cross-subsidies that the power sector is extracting from exporters. Furthermore, the NTDC is seeking wheeling charges at Rs 27/kWh, which is actively “meant to fail the CTBCM model.”

So, to answer those who ask why exports have not increased despite substantial investment in the textile and apparel industry, it is because they are being held hostage by a power sector unable to sustain itself and bent on passing on its own inefficiencies to the rest of the economy. But at what cost?

As power tariffs have increased following the withdrawal of the Regionally Competitive Energy Tariffs regime, textile and apparel production has been reduced by over 50 percent and exports have plummeted. Repeated warnings that deindustrialization is imminent went unheeded to the point that in October 2023, monthly power consumption of textiles and apparel firms on the LESCO network stood at only 114GWh compared to 224GWh in October 2022—a decline of 49%. If the status quo is maintained only to balance the books in the short term, this trend will continue to the point where there will be no export sector left to extract cross-subsidies from.

It must be reiterated that the trajectory of our economy over the coming years hinges on this UoSC determination. Over the next 5 years, Pakistan’s gross external financing requirements—i.e., the difference between all expected inflows and outflows of foreign exchange—are projected at an average of $27 billion annually.

This is the number by which we must increase our annual exports if we are to service our debt and finance our imports without completely drowning in a debt trap in which we are already knee-deep.

“Allowing B2B contracts at a rate of 1-1.5 cents/kWh will provide the export sector with the necessary business environment to work towards this number. It will also facilitate exports in the long run by allowing industry to directly procure electricity from clean sources and achieve net zero emissions that are required to continue exporting to key Western markets beyond 2030.”

Exports cannot be held hostage by policy inaction. Disallowing B2B contracts with wheeling at 1-1.5 cents/kWh will be tantamount to committing economic suicide.