Shahid Sattar and Noreen Akhtar

According to the Global Gender Gap Report 2021, Pakistan ranked 153rd out of 156 countries on the gender parity index and 7th among 8 South Asian countries, doing better than Afghanistan only (Accountabilitylab 2022). Half of Pakistan’s population is comprised of women. If engaged in economic activity, this percentage of the total population is high enough to promote sustainable economic growth in the country. However, Female labor force participation (FLFP) rates in the country are meager (only 23%), particularly in paid employment, representing a massive loss of potential productivity. The low FLFP has implications not only for the country’s economic development but also for women’s empowerment and safety (ADB 2020).

The World Bank Group’s economic memorandum 2022 for Pakistan states that Pakistan experienced some achievement in increasing FLFP rates over the past three decades. It showed an increase from 13 to 24% over the period from 1993-2019 (figure 1). Inter-provincial disparities, however, are high. For instance, Punjab has had higher levels of FLFP than Sindh, KP, and Baluchistan since 1992 (Accountabilitylab 2022).

Pakistan has some success in increasing FLFP over the past three decades

Figure 1: Labor force participation in Pakistan, 1993 – 2019 (World Bank Group 2022a).

Employment expansion for women in Pakistan was driven by an increase in self-employment and unpaid work. Unpaid work rose from 8 to 13% of the female working-age population while paid employment increased from 5 to 11% (mostly self-employment). However, waged jobs for women (better-paid and more productive jobs) remained stagnant since the early 2000s. This brings us to the conclusion that there is an existence of a trade-off between female labor force participation increase and job quality. On the other hand, quality jobs for men rose from 31 to 37% while the overall male labor force participation declined from 83 to 81% of the male working- age population between 1993 to 2019. Female employment was predominantly driven by more agricultural jobs, as the number of male jobs in agriculture declined (Ahmad, 2017; World Bank Group 2022a).

Pakistan has failed to increase female participation in the labor force, while its regional competitors have increased better-paid jobs for their working women to ensure their contribution to economic growth and prosperity. Bangladesh, for instance, has 60% more women in employment than Pakistan (Accountabilitylab 2022). Although similar to Pakistan, female employment in the trade and hospitality sectors is low, Bangladesh has raised female employment in other sectors. This has caused a higher share of Bangladeshi working women in the agriculture, manufacturing, and personal services sectors (World Bank Group 2022a).

The education gap between men and women in Pakistan is larger than in Bangladesh. In Bangladesh, 63% of women and 66% of men have completed at least primary education, while in Pakistan only 35% of working-age women have completed primary education or above compared to 52% of men of the same category. Pakistan, however, has a relatively higher share of people with secondary and tertiary education than Bangladesh. Workers with medium levels of education are underrepresented in Pakistan compared to workers with low or high education levels (World Bank Group 2022a).

Even among women having higher education, only 25% of those participating in the labor force have a university degree, which indicates that women with higher quality education do not enter the workforce after their degree completion, resulting in a significant loss of economic activity. The question ‘why most female university graduates do not enter the workforce in Pakistan’ requires more in-depth research and understanding, as it is crucial for the country to understand the nexus between economic growth and female employment to design policies to achieve greater gender justice (Majid and Siegmann 2021).

GAINS FROM CLOSING FEMALE EMPLOYMENT GAP

If Pakistan closes its female employment gap with Bangladesh, about 7.3 million new jobs would be created. The share of working-age women in employment would rise from 22% in 2018 to 34%. According to ILO, if the gender gap in female participation is reduced by 25% in Pakistan, a GDP rise of 9% is estimated, which is an increase of around $139 billion (Ahmad 2018). Agriculture would be the top sector with the newly created jobs for women (56% of the total increase in employment). Government, personal services, and manufacturing would be the next largest sectoral contributors of new female jobs adding 3.6 million jobs (World Bank Group 2022a). Thus, enhanced FLFP has the potential to significantly boost Pakistan’s GDP.

FLFP IN THE TEXTILE SECTOR

Pakistan’s textile and garment industry employs around 45% of the country’s total labor force. According to the Pakistan Institute of Labour Education and Research (PILER), about 30% of the workers in the industry are women (GIZ GmbH n.d.). Leading textile companies in Pakistan are actively endorsing inclusive and diverse workforce by expanding opportunities for female employees and organizing dedicated technical training for their skill development. The industry is showing a strong commitment to gender equality by devoting efforts to create gender-balanced working teams in the companies. However, in order to effectively close the existing female employment gap in Pakistan, gender balance in employment opportunities at all stages must be ensured on a larger scale in the entire industry.

According to a study conducted by SDPI (2010), women are employed for very few trades in the textile sector (i.e. Stitching and quality assurance) due to low skill development and training. Women experience biased attitudes from employers and very few receive permanent contracts compared to male workers. Provision of female employee benefits such as maternity leaves are not effectively monitored and career progression is comparatively slow in low and medium enterprises.

Japan International Cooperation Agency (JICA) published its Social and Gender Survey Report in 2016-17 for one of its projects on the textile/garment industry. The findings reveal the top three challenges highlighted by the majority of women working in the textile industry. These include lack of transportation, distance from home, and working hours. Moreover, it was stated that female employees expect facilities such as separate toilets, separate workspaces and technical training as they help them perform better in a secure environment but are least considered by the management.

Importantly, the repercussions of the current grave economic crisis and low exports in Pakistan are experienced by the female workers in the textile industry. Many have lost their only source of income while others are paid low wages. Besides, a large number of home-based workers are involved in the industry, who remain deprived of regular capacity development trainings, and other employee benefits. But, with rising requirements on human and labor rights from the international community, the textile industry is increasingly allocating resources to increase female employment and provide a safe working environment and facilities to the female workers.

CONSTRAINTS TO FEMALE LABOR FORCE PARTICIPATION IN PAKISTAN

Social and gender norms

Social beliefs majorly hinder women’s engagement in paid employment in Pakistan. Women are unable to independently decide their participation in labor markets. Women are permitted to work only under exceptional circumstances which include poverty, the so-called acceptable jobs for women, and a progressive mindset within families. In regards to private sector jobs, these are acceptable only if high earnings are to compensate for leaving children unattended and transport costs. Female employment growth in the trade and hospitality sectors is almost zero in Pakistan. Stringent social norms limit women’s participation in jobs that involve high customer contact and shared working spaces with men. It is estimated that overcoming this barrier alone can close the female employment gap by 50% (ADB 2016; JICA 2017; The World Bank Group 2022a).

Mobility

Women experience restrictions on leaving home to participate in the workforce. This concern is widespread among young (15-24 years) and rural women in particular. Thus, the societal norms restricting female mobility may affect around 70% of women in Pakistan. Importantly, what deters women from engaging in activities outside the home is the fear of sexual harassment and discrimination. The lack of transport facilities is another major constraint on women’s mobility. Efficient public transport is available in a few places and private transport options are way expensive (ADB 2016; JICA 2017; The World Bank Group 2022a).

Digital connectivity

Digital connectivity in Pakistan is limited for women. Only 6 and 15% of working-age women reported having used computers and the internet in the past three months in 2019. Access to mobile phones is widespread but with a major gender gap: 30% working-age women compared to 80% working-age men. Low access to affordable internet along with the fear of cyber harassment, lack of necessary digital skills, and stringent cultural norms associated with the use of digital tools has limited the potential of these facilities to support female employment (The World Bank Group 2022a).

Education and skill development

In Pakistan, the gender gap in educational attainment is wide. Around 51% of working-age women in 2018 had never attended school. However, in the case of those who have attended school, educational attainment is similar for both men and women, with higher attainment among women in urban areas. Women with secondary education often lack access to jobs that match their educational attainment and they get involved in unpaid or low-skilled occupations. Women with upper and post-secondary education have high access to wage jobs but limited access to training (The World Bank Group 2022a).

Domestic responsibilities

Women’s participation in the workforce is hindered by the heavy household workloads. This majorly includes childcare burden due to unequal distribution of childcare responsibilities across parents. Women are expected to forego economic opportunities in favor of the so-called respectable domestic roles (Majid and Siegmann 2021; The World Bank Group 2022a).

Home-based work

Between 1993 and 2018, about half of the increase in paid female employment came from jobs performed at home. Pakistan has 4.4 million home-based workers of whom 3.6 million are women. Home-based work has become an acceptable form of female employment in Pakistan, under the continued pressure of domestic responsibilities and social norms. Working from home has its own challenges for women. Home-based workers are the invisible workforce in Pakistan. The burden of work is unhealthy and women despite being full earners online are considered housewives (The World Bank Group 2022b).

Labor demand

Data indicates that gendered occupations are shaped also by employers’ perceptions and preferences for employing women. The belief that hiring women disrupts the workplace exists in five South Asian countries (Afghanistan, Bangladesh, India, Nepal, and Pakistan). In Pakistan, gender segregation is also evident across industries. For instance, 31% to 41% of jobs in the manufacturing, construction, wholesale, retail, hotel and restaurant, transport, storage, and postal sectors prefer male workers (The World Bank Group 2022a).

POLICY RECOMMENDATIONS

- Invest in safe and affordable transport for women, with a focus on female-only transport

- Digital connectivity and digitally-enabled jobs that include increasing access to affordable internet and training on cyber safety and skill development

- Invest in skill development and training programs to consider innovative options to support wage employment opportunities for women with educational attainment

- Existing laws relating to maternity leave and childcare must be enforced and investment in childcare support facilities must be made by the employer organizations in all sectors

- Conditions and opportunities for home-based workers must be improved by providing good working conditions and opportunities for learning and networking.

- Strategies and policies must be developed to support women entering new sectors or traditionally male-dominated sectors, and gender-based discrimination in recruitment as well as workplace harassment must be abolished

- Enforcement of laws against sexual harassment in the workplace, evaluation of their impacts and establishment of communication modes to discourage unsuitable workplaces for women

REFERENCES

Pakistan – Country Economic Memorandum 2.0 (worldbank.org)

Pakistan – Country Economic Memorandum 2.0 (worldbank.org)

https://tribune.com.pk/story/1655699/no-country-working-women

https://www.tandfonline.com/doi/full/10.1080/13545701.2021.1942512

https://www.theguardian.com/global-development/2023/feb/01/pakistan-textile-industry-crisis-women

https://www.jica.go.jp/pakistan/english/office/others/c8h0vm0000brl8b8-att/survey.pdf

https://sdpi.org/gendered-situation-analysis-in-the-textile-sector-of-pakistan/project_detail

https://www.adb.org/publications/policy-brief-female-labor-force-participation-pakistan

Supporting legal reforms to increase women’s workforce participation in Pakistan (worldbank.org)

The gender gap and economic participation of women in Pakistan – Accountability Lab

Shahid Sattar and Noreen Akhtar

Agriculture remains an important sector for Pakistan’s GDP (contributes about 24% of GDP), exports, employment (female employment in particular), and poverty reduction (Pakistan Bureau of Statistics n.d.). Pakistan has shown a stable share of agriculture in GDP over the past three decades, while it has fallen for the aspirational comparators (figure 1).

Share of agriculture in GDP, 1990 – 2020

Figure 1: Pakistan’s share of agriculture in GDP over past three decades, in contrast with comparators (World Bank Group 2022).

Agriculture is a potential sector for poverty reduction in Pakistan, as a larger population share (poor in particular) lives in rural areas. While millions are employed by the sector, the output per worker has been stagnant for three decades and is median among its peers (figure 2). It expanded at an annual rate of less than 0.7% while the average for South Asia expanded four times this rate. This sluggish productivity performance is caused due to distortions created by state interventions that resulted in the resource concentration on four major crops (cotton, sugarcane, wheat, and rice), increased advantage of big landowners and banks at the expanse of small farmers, consumers and future generations and encouraged environmentally unsustainable practices (Ahmed 2020; World Bank Group 2022).

Agricultural value added per worker in constant 2010 US$, 1991-2019

Figure 2: Agricultural value added per worker is low and stagnant in Pakistan relative to comparators (World Bank Group 2022).

PAKISTAN’S VULNERABILITY TO CLIMATE CHANGE

Climate change is an additional risk factor for Pakistan’s agricultural sector. Pakistan is experiencing rates of warming considerably above the global average. The projected data indicates that, even under the optimistic scenario (SSP1-1.9), the annual mean temperature, and number of days with a heat index greater than 35°C are likely to increase for Pakistan. Also, the extreme precipitation events leading to floods, droughts, and sub-daily extreme rainfall events are likely to increase, with much greater risks under the highest emissions scenario (SSP5-8.5) (figure 3) (Almazroui et al. 2020; World Bank Group 2022).

Over 75 million Pakistanis got affected by weather and climate-induced disasters in the past three decades with an estimated economic loss of above US$29 billion (World Bank group 2022). If Pakistan does not adopt the sustainable development scenario, the negative impacts of climate change on human health, ecosystems, and livelihoods will amplify to irreversible levels.

Climate change will, directly and indirectly, alter food production. Directly by altering CO2 availability and temperature and precipitation patterns while indirectly by affecting water availability, seasonality, soil quality and submerging coastal lands, and increasing invasive species. Agriculture will also be affected due to climate-induced impacts on human health and labor force productivity. Further, Pakistan’s irrigation is majorly dependent on the surface water that will experience extreme pressure from climate change (Chaudhry 2017; World Bank Group 2022).

Extreme temperatures have become more common

Figure 3: Projected mean temperatures in Pakistan, reference period 1995-2014, multi-model ensemble (World Bank Group 2022).

*SSPs represent possible societal development and policy paths for meeting designated radiative forcing by the end of the century.

*SSP1-2.6 represents a scenario where GHG emissions (and indirect emissions) are reduced substantially, following the sustainable development pathway

*SSP5-8.5 represents a scenario with very high GHG emissions

CLIMATE CHANGE AND CROP (COTTON) YIELD

According to the Climate Change Profile by Chaudhry (2017), with the rise of 0.5-2°C temperature, Pakistan’s agricultural productivity will decrease by around 8-10% by 2040, with major impacts on the predominant crops.

Regarding cotton yields, higher rainfall, and humidity levels negatively affect these yields. On average, an increase in humidity by 10% leads to around an 8% decline in cotton yields, while a similar increase in precipitation causes a 3.2% loss in yields. The 2022 floods in Pakistan, for instance, caused major losses to cotton with massive spillover impacts on the textile industry, as local cotton constitutes more than half of the industry’s required cotton input. As a result, the industry’s reliance on imported cotton increased while the cotton shortage is still persistent, thus threatening the industry’s sustainable functioning to a large extent.

It is estimated that the 2022 floods have affected around 40% of the annual cotton crop in Pakistan (Russell 2022). The world’s fifth-largest cotton producer is now engulfed by climate disasters with massive losses in cotton and its production. While Pakistan is still a major cotton consumer (third highest among all major cotton-growing countries in 2018) (Pakistan Economic Survey 2017-18), the mounting gap between cotton loss and its consumption has caused devastating economic losses to millions of farmers and the textile industry – Pakistan’s top export industry. The brunt of this economic instability has trickled down to thousands of industry workers whose only source of income is threatened. These challenges are compounded by a lack of research on more climate-resistant cotton varieties and sustainable cotton alternatives for textile manufacturing.

POLICY RECOMMENDATIONS

- Removal of import duties on climate smart-technologies

Climate-smart technologies help address climate-induced disasters including droughts, floods, and heatwaves, which are likely to be intensified in Pakistan. This includes water management strategies such as alternative wet and drying or laser leveling to increase productivity. Likewise, renewable energy (RE) technologies including windmills and bio-energy production units can be used for efficient water supply and storage and to power farm equipment.

Climate-smart technologies are subject to high import duties that have increased their domestic price and made them less feasible for adoption. As Pakistan’s major industries including the textile industry are experiencing mounting sustainability requirements from the global community of buyers including EU, these import duties need to be abolished in order to enable the industries reduce their carbon and water footprint by adopting these technologies.

- Investment in enabling services to connect farmers to markets and enhance their capabilities

Connectivity enhances agricultural productivity and farmers’ incomes by connecting them directly to the markets. In the case of Pakistan, cellphone access helps farmers to move cash crops as it improves timely coordination with traders at the time of harvest, thus minimizing loss. Therefore, both hard and soft connectivity is crucial to facilitate connectivity and information provision to farmers.

- Improvement in the innovation ecosystem, facilitate university-private sector and public-private sector linkages and increase R&D investment

This development is crucial to ensure sustainable growth in agriculture but also to promote research on more climate-resilient crop varieties such as cotton and their sustainable alternatives. This is also important to shift Pakistan’s reliance from only few major crops to a wide variety of crops that can be cultivated to overcome food insecurity in the country.

- Monitoring of sustainable farming practices

Farming practices in Pakistan must be regulated to avoid GHG emissions, unsustainable water consumption patterns and use of environmentally unhealthy inorganic fertilizer. This is necessary to avoid land degradation – an already major environmental challenge in Pakistan that has affected land productivity.

(World Bank Group 2022)

REFERENCES

Pakistan – Country Economic Memorandum 2.0 (worldbank.org)

https://www.just-style.com/news/pakistan-floods-hit-40-of-annual-cotton-crop/

https://link.springer.com/article/10.1007/s41748-020-00157-7#citeas

https://www.pbs.gov.pk/content/agriculture-statistics

https://macropakistani.com/agriculture-in-pakistan/

https://www.adb.org/sites/default/files/publication/357876/climate-change-profile-pakistan.pdf

https://www.finance.gov.pk/survey/chapters_18/02-Agriculture.pdf

Shahid Sattar and Ureeda Majeed

While inflation has become a major topic for debate in today’s world politics, it is actually a tale as old as time. The world’s first recorded hyperinflation came during the French Revolution, During the 20th century, seventeen hyperinflations occurred in Eastern Europe and Central Asia, including 5 in Latin America, 4 in Western Europe, 1 in Southeast Asia and one in Africa. The US came close twice – during the Revolutionary War and Civil War – when the government printed currency in order to pay for its war efforts. As it turns out throughout history hyperinflation usually coincided with wars, natural disasters and a series of ill-advised fiscal and monetary policy decision but at the core is a result of a rapid increase in the money supply that is not supported by growth in the economy.

Inflation can either be cost push (occurs when prices rise because production costs increase, such as raw materials and wages) or demand pull (caused by strong consumer demand for a product or service). Another form of inflation is defined as Built-in inflation which occurs when enough people expect inflation to continue in the future. Because of these shared expectations, workers may start to demand higher wages in order to anticipate rising prices and maintain their standard of living. Increased wages would result in higher costs for businesses, which may pass those costs on to consumers. Higher wages also increase consumers’ disposable income, increasing the demand for goods that can push prices even higher. A wage-price spiral can then be set in place as one factor feeds back into the other and vice-versa.

Today world’s inflation is being driven by high consumer demand and low supply in the economy. After the pandemic restrictions loosened up, the demand for goods skyrocketed while the supply couldn’t keep pace along with war in Ukraine causing further interruptions to the supply chain and increases in the prices of oil and food.

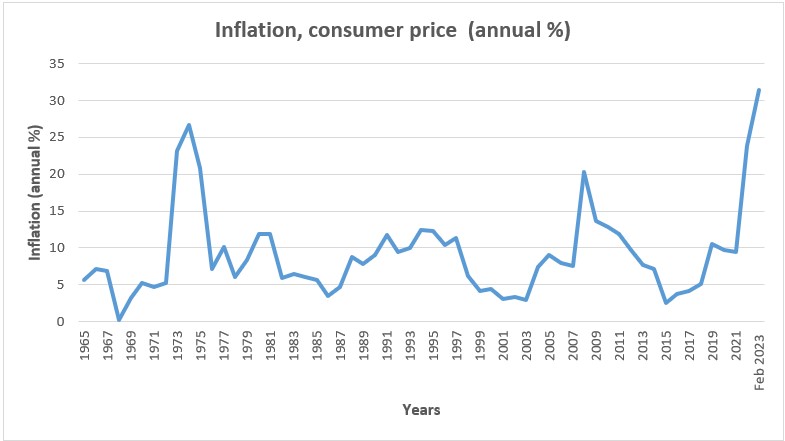

According to PBS Pakistan’s consumer price inflation jumped to 31.5% in February of 2023, the highest rate since June of 1974, following a sharp depreciation in the rupee and as the government announced a rise in energy prices and taxes to meet the International Monetary Fund’s loan conditions. At the same time, the consequences of last year’s devastating floods have accumulated economic difficulties. FAO in its recent “Food Security Update” attributes the high prices to generally stagnant production since 2018, stock losses and disrupted trade flows due to the 2022 floods, high agricultural input and transportation costs, and high headline inflation. Inflation in the developing world is mainly linked to import dependence. As the dollar goes up imports become more expensive. As exports rely on imports, exports don’t become competitive despite declining of rupee which leads to more devaluation and more inflation. With the high inflation state bank have to push up the discount rate to restrict the supply of money which slows down the economy. The cost of working capital for exporters increase and finances are not available for exporters due to increased interest rates as a result exports do not increase with the devaluation of rupee.

(Data Source: World Bank)

The State Bank of Pakistan is raising interest rates to make lending and investing more expensive through its monetary policy in order to imprison the inflation gennie back in the bottle. However, this text book solution might not work well for an economy like Pakistan. Raised interest rates can easily impact the labor market, causing unemployment levels to rise. Inflation in Pakistan is cost push and most important components of our Consumer Price index (CPI) are Food, Housing, Water, Electricity, Gas & Other Fuels, Clothing & Footwear, and Restaurants & Hotels. All of which remain unaffected by changes in interest rates. Higher interest rates are unable to do anything about supply chain issues (such as shortage of wheat or ghee which may give rise to food inflation or shortage of cotton) that cause inflation to rise. The cost of food, housing and clothing and foot wear will continue to increase irrespective of interest rates and consumers’ basket will continue to become more expensive with standards of living continuing to decline.

At the same time the government is using fiscal policy to fix inflation by increasing taxes or cutting spending. Principally, increasing taxes leads to decreased individual demand and a reduction in the supply of money in the economy. However, taxing electricity, gas and fuel increases the cost of manufacturing for the industrial sector making our producers uncompetitive. Instead of fostering and nourishing healthy business and entrepreneurial practices the policies at present are stifling the economy. This burden of the increased cost is then transferred to the consumer through higher prices which further increases inflation. The increased taxes on energy are not only increasing household energy bills but also aggravating the situation by further increasing the cost of final goods and services thus overall again increasing the cost of consumer’s basket and decreasing the purchasing power of individuals.

Perhaps the most devastating fact remains that the rationale behind increasing taxes and interest rates is to decrease demand however no matter how much the taxes are raised the aggregate demand of the country continues to increase because of the increase in general population. As our population continues to grow it is putting immense pressure on whatever’s left of the dwindling resources of Pakistan. The demand for petroleum of Pakistan is inelastic in nature so increasing interest rates has no effect on its demand and consequently the economy continues in a downward spiral and inflation keeps on increasing.

As every morning the stock market awaits the finalization of the IMF bailout package only to be disappointed again and again, the economic crises in the country is constantly intensifying. With increasing political instability and declining reserves the country is on the brink of bankruptcy. While the ban on imports persists, with the consignments of raw materials stuck at ports the country awaits the release of $1.2 billion tranche from the IMF.

When the government increases the interest rates the government who itself is the lender of last resorts becomes the borrower. Pakistan’s government debt jumped by PKR 4 trillion or around 7.7% in January 2023 to reach close to PKR 55 trillion. Meanwhile, domestic debt rose to PKR 34.3 trillion by January end. The high interest rates only serve to raise country’s own costs. In order to finance this debt, the government will have to continue to increase taxes and the will economy shrinks further. According to Moody’s Analytics inflation in Pakistan could average 33% in the first half of 2023 before trending low and a bailout from the IMF is unlikely to put the economy back on track.

PAKISTAN’S DEBT AND LAIBILITIES – SUMMARY (in Billion PKR)

| Jun-22 | Dec-21 | Sep-22 | Dec-22 | |

| I. Government Domestic Debt | 31,037.5 | 26,746.5 | 31,404.6 | 33,116.3 |

| II. Government External Debt | 16,747.0 | 14,796.5 | 18,004.5 | 17,879.8 |

| III. Debt from IMF | 1,409.6 | 1,188.4 | 1,731.4 | 1,724.8 |

| IV. External Liabilities | 2,275.6 | 2,055.0 | 2,440.3 | 2,486.5 |

| V. Private Sector External Debt | 3,596.3 | 3,029.6 | 3,900.3 | 3,799.2 |

| VI. PSEs External Debt | 1,675.7 | 1,205.3 | 1,805.8 | 1,792.3 |

| VII. PSEs Domestic Debt | 1,393.4 | 1,503.8 | 1,470.4 | 1,474.3 |

| VIII. Commodity Operations | 1,133.7 | 889.4 | 1,126.8 | 1,138.8 |

| IX. Intercompany External Debt from Direct Investors abroad | 905.1 | 785.0 | 997.5 | 931.2 |

| Total Debt and Liabilities (sum I to IX) | 59,698.9 | 51,725.6 | 62,406.6 | 63,868.2 |

| Gross Public Debt (sum I to III) | 49,194.0 | 42,731.4 | 51,140.5 | 52,720.8 |

| Total External Debt & Liabilities (sum II to VI + IX) | 26,609.2 | 23,059.8 | 28,879.8 | 28,613.8 |

(Source: State Bank of Pakistan)

The policy instruments used by the government are just not working and while the interest rates and taxes are increasing inflation in Pakistan continues to rise. One reason for why Pakistan is trapped in high inflation and interest rates spiral may be the structural issues in Pakistani markets. Pakistan’s economy is haunted by ineffective market mechanism causing disruption to already volatile and sensitive supply chains which are susceptible to environmental changes and economic and political instability. Unstable Markets are prone to shortages and surpluses. The matter is worsened by inelastic demand and consumption patterns which are deeply rooted in our culture and spending habits which cannot be changes overnight.

The old belief that invisible hand of the market will ensure efficient allocation is no longer in play because there are discrepancies in our system which prevent optimal allocation and efficiency. The government cannot rely blindly on market powers to play out anymore. Instead of the invisible hand of the market what we need is perhaps a very visible hand of the policy makers to rescue the country out of this spiral of low growth and increased inflation. Government should immediately reduce the discount rates and let the economy breathe so that it naturally breaks free of this whirlpool of inflation. A controlled intervention by the government by reducing its spending would tamp down on demand-fueled inflation, while at the same time restoring confidence in the ability of the federal government to pay down the debt and thus control inflation expectations. Policies such as reduction in import duties of critical raw material used for production will result in stability of final price of goods and services. Government can help control inflation by reducing tariffs and nontariff barriers that push up the price of goods, ending regulations that boost shipping costs, and encouraging production of renewable energy among other means. It can reform tax laws to increase tax base. The government can take practical steps towards making supply chains and demand systems more seamless and less prone to disruptions while promoting a healthy culture of savings and investments.

Where We Are