Shahid Sattar and Eman Ahmed

Amid elevated levels of inflation, the war in Ukraine, and rising interest rates, global economic growth is expected to be weak in 2022 and 2023. The war has resulted in elevated prices of food and energy, and the situation is increasingly dire. Being an oil importing country, Pakistan heavily relies on hard currency to finance imports, and is thus faced with mounting food and energy prices and deteriorating external balances.

Central banks across the world have been raising interest rates to tame inflation, but this monetary policy fails to account for supply shock disruptions. Pakistan’s interest rate remains elevated at 15%, thereby hurting businesses and stifling investment and entrepreneurship. The annual inflation rate increased to 24.9% in July 2022, the Pakistan Bureau of Statistics reported.

Pakistan’s interest rate has intentionally been maintained at a high level in miscalculated attempts to control inflation, by means of a contractionary monetary policy. Although policies of this nature have been effective in reducing inflation for certain Highly Developed Economies, there is no evidence to suggest the same rules apply to the case of Pakistan. On the contrary, it is proven that a high interest rate in Pakistan leads to an increase in cost-push inflation. This belief was echoed by Nobel laureate economist Joseph Stiglitz, who recently described how within the US economy and others possessing market power, companies can afford to raise prices without losing business. Meanwhile, standard economic models suffer from even more inflation when subjected to rate hikes.

Contractionary monetary policy operates by decreasing the money supply in order to increase the cost of borrowing. This measure normally decreases GDP and dampens inflation. The State Bank chose to maintain a high interest rate, decreasing the money supply in attempts to curtail inflation. However, the opposite impact has been observed in Pakistan’s case, as here there is a directly proportional relationship between inflation and discount rate.

Former federal minister for finance Dr. Hafiz Pasha has said that focusing on export-led growth, increase in tax-to-GDP ratio, revenue collection from the untaxed and a crash programme for the loss-making state owned enterprises are a must to get rid of the economic challenges being faced by the country. He added that in the absence of FDI, if the government decides to issue bonds, it would have to issue at 22 percent interest rate, which, of course, would be untenable.

Though Pakistan is a resource-rich country, its economic condition is deteriorating, and Dr. Pasha fears that the country’s foreign exchange reserves could go down below $7 billion before receiving money from the IMF. He opined that a safe level is $18-19 billion.

Public debt in July was around Rs50 trillion while the external debt-to-GDP ratio reached 41%. Five years ago, external loans stood at $83 billion, which are $130 billion today. “It is a matter of concern that we do not have foreign exchange reserves at the beginning of the financial year.”

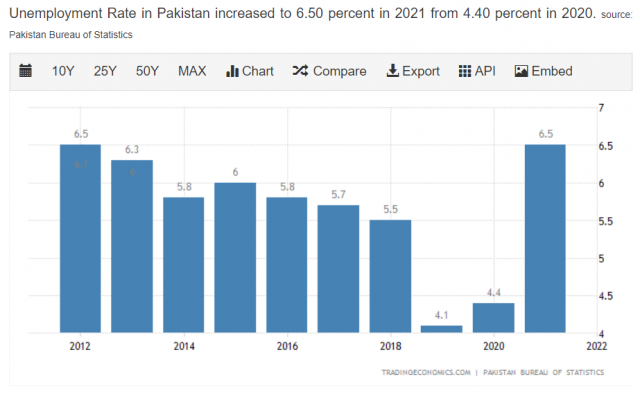

Investopedia defines stagflation as “the simultaneous appearance in an economy of slow growth, high unemployment, and rising prices.” In Pakistan, growth is expected to moderate from 5.7 percent in FY2020/21 to 4.0 percent in 2022/23 as foreign demand slows significantly and policy support is withdrawn to contain external and fiscal imbalances. (World Bank) The annual inflation rate in Pakistan increased to 24.9% in July of 2022, the highest since October of 2008, amid a slide in the rupee to record lows. Furthermore, according to PIDE, over 31% of Pakistan’s youth are currently unemployed, out of which 51% are females, 16% are males, and many of whom hold professional degrees.

Inflation in Pakistan

Unemployment Rate in Pakistan

Unemployment Rate in Pakistan

For a country like Pakistan where the major export is textiles, the economy largely relies upon low-value and geopolitically insignificant products. Investment in machinery for value addition is also stagnating in the face of present economic turmoil. To strengthen the trade value of a small economy like Pakistan, there is a need for enhanced trade openness. This necessitates the identification of efficient trade routes and diverse networks of supply chains to ensure smooth flows of goods and materials. It requires tighter integration and communication between supply networks which should be coordinated between both public and private sectors.

However, these matters have been further aggravated due to the State Bank’s failure to approve critical imports of textile mills in a timely manner. Payments for essential inputs are not being approved due to unnecessarily bureaucratic procedures and delays at the provincial level. These delays pertain to imported machinery parts which are regular inputs for textile machines – essentially required to run and maintain spinning and weaving machines. The situation is dire, as without timely supply of spare parts to the machines, production is halted indefinitely. This is leading to massive and unrecoverable losses of exports, and further restricting economic growth.

Meanwhile, MENA oil exporting countries are forecast to witness their highest growth rates in 2022 (Figure 5). This is primarily due to higher oil prices and almost complete recovery from the pandemic due to residents’ high vaccination rates. However, higher oil prices may slow down the urgency of the past ten years to: (i) transition to renewable energy sources; (ii) diversify the economy away from oil; (iii) reduce the role of the public sector in the economy. (Whiteshield)

Moreover, industries in Pakistan are energy intensive and will therefore see rising input costs of energy, other commodities and borrowing. With interest rates being synchronized with the US Fed policy interest rates, borrowing and servicing debt costs are expected to rise. Furthermore, the strengthening value of the US dollar has been constricting the textile industry’s liquidity and eroding competitiveness.

In this high-risk scenario, it is recommended that stress tests and policy assessments be undertaken at the highest levels of government. “The over-riding objective is to forge crisis-specific resilience and stabilization plans that help developing countries wither the gathering global economic storm.” (Whiteshiled) An export-led economic growth model is central to strengthening these economies, but this also requires a more diversified product basket and diversified markets. The major exports of textiles need to be supported for value addition while simultaneously tapping into other products and services. This is more sustainable than acquiring more foreign aid.

Higher value addition through technology, IT investment and renewable energy generation are the most impactful and symbiotic means to improve the economy while simultaneously enhancing worker capabilities and enabling integration into Global Value Chains. Enhancing internal capacity in these industries will allow is to reduce imports. Pakistan’s import bill has historically been weighed down the most by petroleum imports; therefore, drives for domestic exploration of renewable energy sources must be introduced, and the transition to solar and wind capacity must be pursued aggressively, which will have positive impacts on job creation and skill enhancement for the population.

If we target the doubling of Pakistan’s trade value by 2030, there is a need for aggressive export facilitation by the government by incentivizing exports and reducing tariffs for the most productive and high potential exporting industries, and by reviewing non-tariff barriers to trade and ensuring international standard compliance. The country should engage professional consultants to lobby for GSP+ status for Pakistan. With our competitive advantage in textiles, Pakistan should be able to target 10-15 leading brands and retail chains in the USA and Europe for sourcing Textile & Clothing from Pakistan.

It is often argued that giving priority and subsidies to exporters will lead to neglect of other industries and businesses such as local startups. However, this is the most effective geo-economics strategy for a country like Pakistan that struggles to in forex through other sustainable means, so these measures are critical for the long-term stability of the economy. Another strategic implication to bear in mind is that reducing oil imports may result in energy shortages if domestic production is not able to keep pace. Since exports are to be supported on a priority basis, this may lead to power cuts for domestic consumers and industries that are less productive, resulting in energy insecurity in the short term. However, the strategy of prioritizing domestic energy is not geo-economically prudent and is more often applied for political gain e.g. to secure votes.

The textile industry has definite advantages for Pakistan’s economy – it is labor intensive, easy to set up and expand, has low skill requirements using simple machines and processes. There is a high demand, a large market and fast profits. Furthermore, it supports many advanced derivative industries including dyeing, chemicals and design. It is therefore a gateway industry into making an economy capital-rich and possibly geo-economically significant. However, value addition and progress are the ultimate goal for economic growth. Strengthening domestic production of energy, hi-tech, finance, media and communications, strategic materials and healthcare are what make a strong and powerful economy. To achieve this, we must reduce the high government footprint in Pakistan’s economy, as it limits ability for private businesses and free market forces to enable growth and diversification, and we fall prey to a boom-and-bust cycle where short and stunted growth cycles are followed by periods of stagnation, particularly vulnerable to global shocks and disruptions.